Highlights

Regular reviews of term insurance are vital. Adjust coverage with life changes. Check nominee details & tax benefits.

Latest news

Emma Roberts to return for 'Aquamarine' TV series 20 years after original film

IBM unveils first sub-1 nm chip; Packs nearly 100 bn transistors into a space the size of fingernail

ZTE Showcases Full-Stack AI Capabilities at MWC Shanghai 2026, Empowering New Era of Token Operations

Tailorworks Introduces a Modern Approach to Bespoke Fashion for Today's Luxury Consumer

Zoey Deutch says having two Taylor Swift songs in 'Voicemails For Isabelle' "meant a lot" to her

PNB MetLife records 99.81 percent Individual Claim Settlement Ratio in FY26

"India-Israel FTA may be signed in very near future": Israel Embassy's Economic Division head Ofir Amami

When Should You Review Your Term Life Insurance Policy?

When Should You Review Your Term Life Insurance Policy?

VMPL

New Delhi [India], June 26: Buying a term life insurance policy is a strong first step. Reviewing it is the part that keeps it relevant. Income changes, loans get added, children grow, parents age, and financial goals become sharper. A policy bought at 28 may still be active at 38, but the household around it may have changed completely. That is why a review is not a sign that the first purchase was wrong. It is simply how a responsible financial plan is kept in working condition.

Many people review investments every few months but leave insurance untouched for years. Maybe because insurance feels settled once the policy document arrives. But term insurance is linked to responsibilities, and responsibilities are rarely still. A practical review every few years, and after major life events, helps the cover remain aligned with real needs.

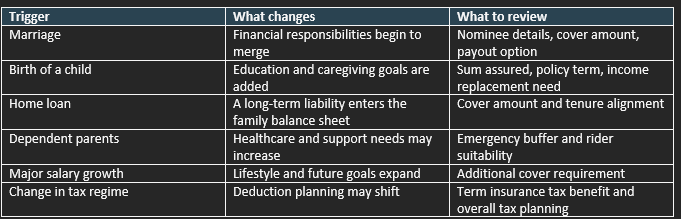

Review after a meaningful increase in income

Income growth changes the standard of living of a family. Expenses rise, future goals become larger, and sometimes loans become bigger too. If your income has moved up substantially since the time you bought the policy, your existing cover may need a fresh calculation.

This is especially important for people who bought a basic cover early in their career. A Rs. 50 lakh policy may have looked adequate when income was modest and there were no dependents. A few years later, with a home loan, spouse, child, and higher monthly expenses, the same policy may need to be supplemented. The review should look at the gap calmly, not dramatically.

Life events that should trigger a review

Review your nominee and contact details

This sounds small, but it is not small at claim time. Nominee details should be correct, complete, and updated after marriage, divorce, death in the family, or any change in family arrangement. Mobile number, email ID, and address should also be current. A policy that cannot be serviced smoothly because basic details are old creates avoidable work later.

A good habit is to check nominee and contact details at the same time as you download the annual premium receipt. It takes a few minutes. It keeps the document alive in a practical sense.

Review when you take a large loan

A home loan is usually the biggest reason to revisit term cover. The family should not have to handle a long repayment burden without the earning member's income. If the loan is large, a top-up policy or an additional term plan can be considered. Some people prefer a separate cover linked mentally to the loan, even if not formally assigned to it, because it gives clarity to the family.

- Check outstanding principal, not the original loan amount.

- Match the cover period with the loan tenure where practical.

- Tell the nominee how much of the claim amount should be used to close or reduce the loan.

- Review again if you prepay the loan aggressively or take a top-up loan.

Review riders and payout options

Riders chosen at purchase may still be useful, but your needs can change. A critical illness rider, waiver of premium benefit, or accidental benefit may need to be assessed against your current employer benefits, health cover, savings, and family situation. The point is not to keep adding features blindly. The point is to know what each feature is doing for the plan.

Payout design also deserves attention. A lump sum may be right for some families. Others may benefit from a regular income option or a mix of lump sum and income, where available. If your nominee is comfortable managing money, the decision may be different from a family where structured income would provide more order.

Review tax treatment, but do not make tax the only reason

Term insurance tax benefit can be relevant while planning annual finances. Premiums may qualify for deduction under Section 80C subject to conditions, and claim proceeds may be eligible for exemption under Section 10(10D), again subject to applicable rules. Since tax provisions can change and eligibility depends on the policy and taxpayer profile, it is better to verify before filing returns.

Still, term insurance should not be reduced to a tax-saving purchase. Its main role is protection. The tax benefit is useful, but the cover amount, nominee readiness, policy term, and continuity of premium payment carry deeper importance.

A quick review checklist

1. Is the current sum assured enough for loans, expenses, and goals?

2. Does the policy term cover the years of highest responsibility?

3. Are nominee and contact details updated?

4. Are premium payments running smoothly?

5. Do riders still fit your current financial situation?

6. Is the payout option suitable for the nominee?

7. Have tax details been checked for the current financial year?

Final view

A term life insurance policy should be reviewed whenever life becomes financially bigger: higher income, bigger loans, children, dependents, or a change in tax planning. Even without a major event, a review every two or three years is sensible. The policy then remains connected to the household it is meant to protect, instead of becoming an old document stored somewhere and remembered only at premium time.

(ADVERTORIAL DISCLAIMER: The above press release has been provided by VMPL. ANI will not be responsible in any way for the content of the same.)

Up Next

When Should You Review Your Term Life Insurance Policy?

Step-by-step guide to apply for a mortgage loan online with minimal documentation

Honda Activa 6G: Everything You Need to Know Before Buying

How much does a ULIP plan really cost? A break-down of all charges

Centre plans to borrow Rs 8.20 lakh cr from market in first half of FY27

Reliance denies buying Iranian oil amid US sanctions waiver

More videos

Premium petrol price up Rs 2, industrial diesel up Rs 22; no change in normal petrol, diesel rates

India's GDP expected to register over 8 pc growth in Sep-Dec: Report

Govt announces seven measures to help boost exports

RBI keeps interest rates on hold after US trade deal boosts outlook

RBI proposes to compensate customers up to Rs 25,000 loss due to fraud

RBI raises GDP growth projection of Q1, Q2 of FY27

RBI pauses rate cuts, retains interest rate at 5.25 pc

Rupee jumps 122 paise to close at 90.27 against US dollar on India-US trade deal

Stock markets cheer India-US trade deal: Sensex, Nifty surge 2.5 pc

UPI transactions hit record high of Rs 230 lakh crore in 2025-26 till Dec: Govt